Contents

As 2026 approaches, risk conditions are shifting faster than many businesses can adapt.

A new analysis by global financial authority Moody’s (Insuring Tomorrow: 10 Emerging Risks) highlights 10 emerging threats expected to reshape insurance markets worldwide. While these are global trends, they may have direct, costly implications for your business and property here in Australia.

From climate extremes to “forever chemicals,” here is what you need to monitor to protect your Australian operations in the year ahead.

1. Climate Exposure: Will the Cost of “Paradise” Rise for You?

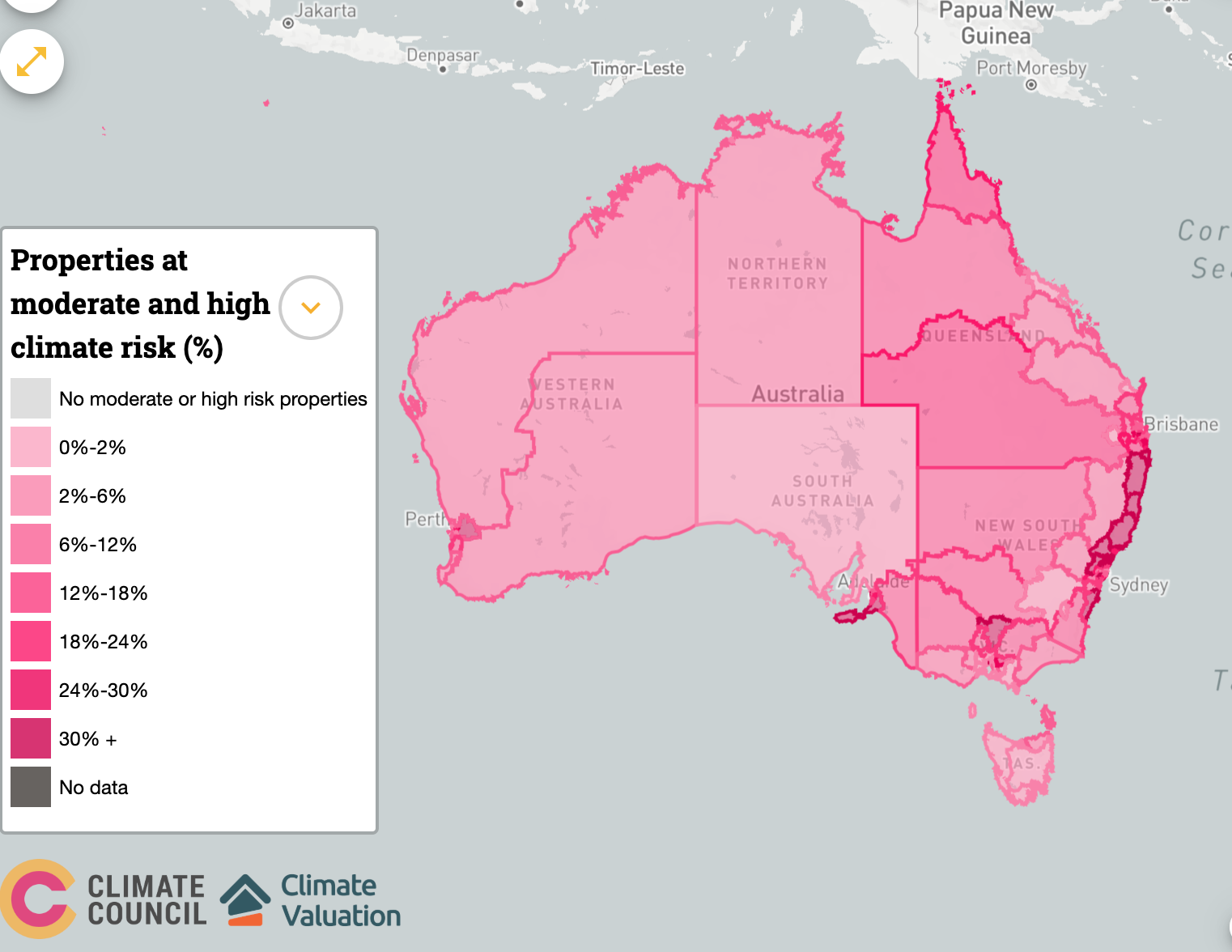

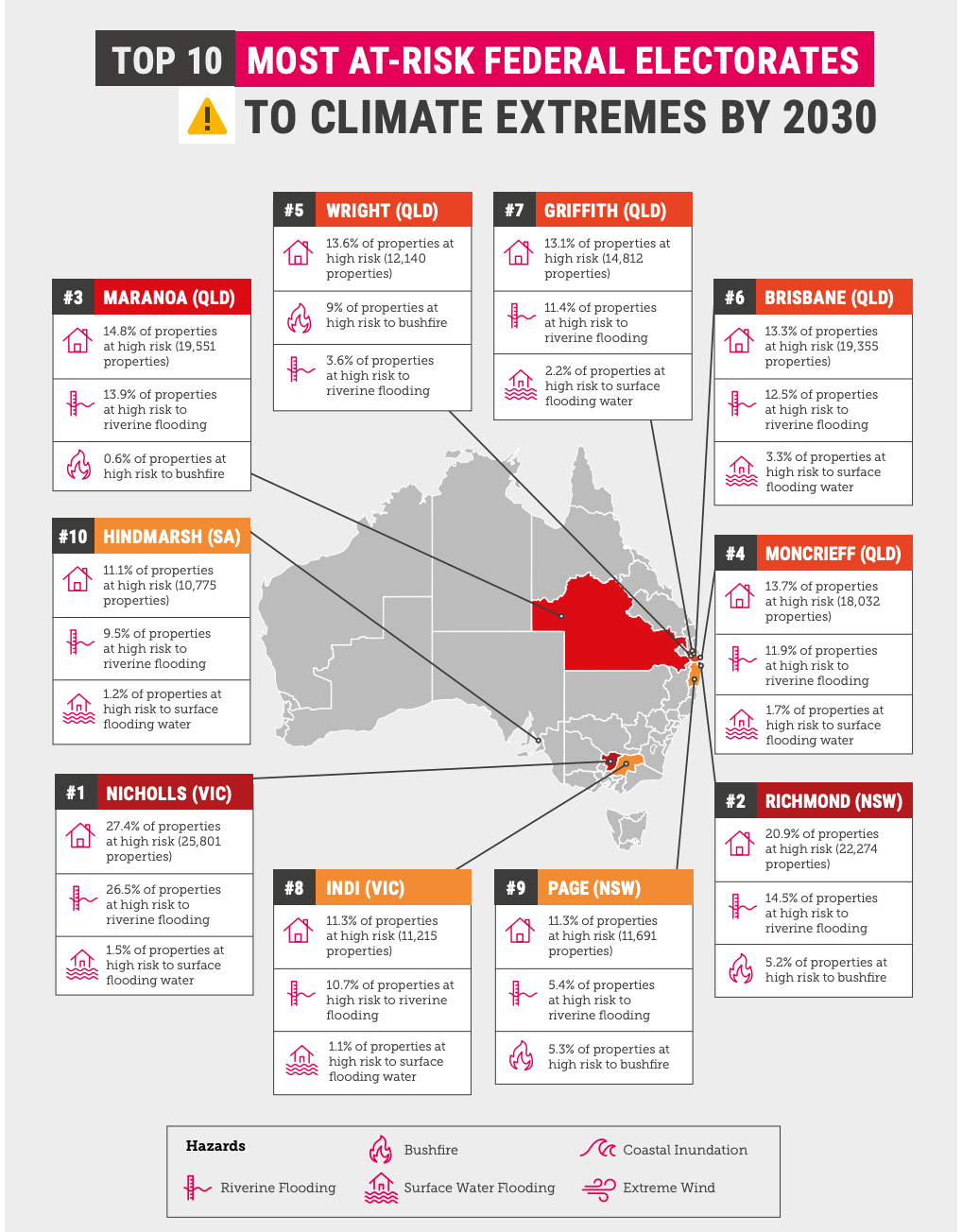

The Short Answer: Yes. Sea-level rise and severe weather are redefining risk in areas once considered highly desirable, such as coastal suburbs and riverfront towns.

The Report Warns: Property in high-amenity environments now carries rapidly increasing insurance costs due to intensifying storms, coastal erosion, and flood frequency.

## How does this affect your Australian business?

If your premises are in a high-exposure zone, particularly in Northern NSW (Richmond, Page), Brisbane, the Gold Coast, or Regional Victoria (Nicholls), expect this to be the primary driver of premium increases.

The Climate Council warns that 1 in 25 properties across Australia will be effectively “uninsurable” by 2030, with riverine flooding causing 80% of this risk. Insurers are now using strict “address-level” data to model this, meaning two businesses on the same street can see vastly different premiums based on specific elevation and flood exposure.

2. Supply Chain Fragility: Is Your Business at Risk of Interruption?

The Risk: Supply chain breakdowns remain a critical threat. The Allianz Risk Barometer 2025 ranks Business Interruption as the #2 Global Business Risk, driven by geopolitical conflicts, shipping tensions, and the “ripple effects” of natural disasters.

While Australian businesses are increasingly worried about regulation (our local #2 risk), the global supply chain crisis hits our shores in two very specific, costly ways:

What this means for you:

- Longer Repair Times: The “supply chain” for repairs is broken. A national shortage of over 28,000 skilled technicians means that if your work vehicle or machinery is damaged, it could be off the road for weeks, not days. You aren’t just waiting for parts; you are waiting for the people to fit them.

- Sum Insured Gaps: Disrupted supply chains drive up the cost of materials. Construction costs have surged 30.8% since the pandemic began. If you haven’t updated your “Sum Insured” to match 2026 replacement values, you are likely insuring a building that no longer exists at that price point.

3. Pandemic Potential: A Warning on Exclusions

The Risk: While COVID-19 fatigue is real, Avian Influenza remains a top-tier threat on the global risk register. While Australia is currently free of the H5N1 strain causing havoc overseas, authorities are on high alert for its arrival via migratory birds.

Your Insurance Implications: Do not assume you are covered for a new pandemic. Following the COVID-19 court battles, almost all Australian Business Interruption (BI) policies now explicitly exclude diseases listed under the Biosecurity Act 2015.

The Reality: If a bird flu outbreak triggers lockdowns or trading restrictions in 2026, standard insurance policies will not cover your lost income.

What you should do: Review your Business Continuity Plan to ensure your business can survive a shutdown without insurance support.

4. “Wandering” Wildfires: Are You Safe in the Suburbs?

The Risk: Wildfires are expanding into regions not previously considered “high risk.”

Australian insurers are now closely modelling the “rural-urban interface,” where fast-moving grassfires and long-range embers can destroy homes kilometers away from the actual fire front.

Why this matters to you:

- The “Ember Attack” Penalty: Research shows that 90% of houses lost in bushfires are destroyed by ember attacks, not direct flame contact. Insurers use “address-level” modelling to rate this risk.

If your business is on the urban fringe (e.g., Western Sydney, Perth Hills, or Melbourne’s North), you may face “bushfire zone” premiums even if you are on a standard suburban street.

- The “BAL” Rebuild Trap: If your property is damaged, you must rebuild to current Bushfire Attack Level (BAL) standards. These strict codes (requiring fire-rated glazing and timber) can add $30,000–$100,000+ to a rebuild cost. If your sum insured doesn’t account for this extra compliance cost, you are effectively underinsured.

5. “Insuring Nature”: How Will This Long-Term Shift Affect You?

The Risk: There is a rising strategic focus on “nature-based” risk mitigation such as restoring wetlands to absorb floodwater or urban forests to lower heat intensity.

The Shift for You: While planting trees won’t lower your premium overnight in 2026, it is fast becoming a deciding factor in community-level insurability. If your suburb lacks these natural defences, insurers may view the entire area as “too exposed” in the future.

The Evidence: The Insurance Council of Australia (ICA) and major insurers are now actively lobbying for “Nature Positive” infrastructure (like mangroves and dunes). They view these assets as essential barriers to keep high-risk Australian regions insurable.

Alt text: Aerial view of a vibrant green mangrove forest ecosystem bordering turquoise tidal waters. Used to represent environmental assets, coastal protection, or climate change impact on natural habitats.

Your Action Plan: If your local council proposes green infrastructure projects, support them. These community-level defences are becoming the only way to keep insurance capital available for your property in the long run.

6. Fast Floods: How Will Extreme Rainfall Affect Your Policy?

The Risk: Intense rainfall events are accelerating. “Flash flooding” is now affecting suburbs, deserts, and infrastructure networks that historically felt safe.

The Local Impact on You: Australia’s East Coast Lows make this a headline risk, often dumping months of rain in hours.

What you should do:

- Policy Check: Does your policy cover “Flood” (rising water from a watercourse) or just “Storm” (rainwater runoff)?

- The Trap: In a heavy downpour, “Storm” (runoff) often mixes with “Flood” (overflowing creeks).

If you only have “Storm” cover, insurers may deny the entire claim if they can prove a nearby creek contributed to the inundation. In 2026, having clear Flood cover is the only way to avoid these technical disputes.

7. Cyber Outages: Is Your Third-Party Risk Covered?

The Risk: The 2024 CrowdStrike outage was a wake-up call. Industry reports warn that third-party system failures, vendors you rely on but don’t control, are becoming a dominant exposure for Australian businesses.

## Are you at risk?

This is highly relevant if you run an Australian SME, health practice, or logistics firm reliant on cloud software.

Warning: Many basic Cyber policies cover malicious attacks (hacks) but exclude or limit cover for non-malicious system failures (like a software update crashing your system).

- The Market Shift: Following CrowdStrike, insurers are becoming “more cautious” with this coverage. The Cyber Insurance Market Update 2025 warns that insurers are now removing “blanket” system failure clauses or applying stricter sub-limits and carve-back.

2026 Outlook: Underwriters may ask strict questions about your vendor management. Legal experts warn that “third-party diligence” is now a key compliance focus for 2026, meaning insurers will want proof you are monitoring your suppliers before they insure you for their failures.

8. High-Risk High-Rises: How Does Density Affect Your Assets?

The Risk: Rapid urbanisation is driving high-density construction, but the legacy of the “building boom” is a massive defect bill estimated by the Insurance Council of Australia at $1.3 billion annually.

## How does this affect you?

The Australian strata market has split into two speeds.

- The Good News: For well-maintained buildings, the market has stabilised. The CHU 2025 State of the Strata Market Report confirms that average premiums rose just 2.8% in 2025.

- The Trap: If your building has unresolved maintenance or defects (like waterproofing issues), insurers are taking a hard line.

Industry updates warn that these properties may face steep premium hikes, higher excesses, or total refusal of cover until specific engineering reports prove the defects are fixed.

9. “Chemicals Forever”: Could You Face Liability for PFAS?

The Risk: PFAS (synthetic “forever chemicals”) are now a priority regulatory target. As of July 1, 2025, the Australian Government officially scheduled these chemicals for phase-out under the IChEMS Register.

What you need to watch: Insurers are responding faster than businesses.

- The Exclusion: Major insurers are actively adding “Absolute PFAS Exclusions” to General Liability policies in Australia.

- The Impact: If your business touches manufacturing, transport, or waste management, check your renewal policy. If you are sued for environmental contamination linked to PFAS 10 years from now, your current policy might explicitly exclude the claim, leaving you personally liable.

10. Microplastics: Are You Prepared for the Next “Asbestos”?

The Risk: Moody’s warns that microplastics present the next frontier in casualty insurance, potentially mirroring the scale of asbestos litigation in future decades.

Alt text: A close-up photograph of microplastics

Future Liability for You: This is an emerging “long-tail” risk.

- The Outlook: Reinsurers and legal firms are already advising underwriters to tighten exclusions and demand rigorous disclosures from plastics and food packaging manufacturers.

- Action: Expect your insurer to start asking detailed questions about your product lifecycle. If you cannot prove you are tracking microplastic shedding or contamination, you may find your Product Liability cover restricted in future renewals.

What These Risks Mean for Your Business in 2026

While the global risk landscape remains complex, the local Australian market is shifting in favour of businesses but only for those with the “right” risk profile.

The Short Answer: If you have a standard risk profile, you can expect lower premiums. If you are in a “distressed” sector (like strata with defects), conditions remain tight.

## 1. Will Your Business Insurance Rates Drop? (The “Two-Speed” Market)

Contrary to the global trend of rate hikes, Australian businesses are currently seeing the largest price drops of any region globally.

According to the Marsh Pacific Insurance Market Index (Q3 2025), commercial rates in the Pacific region declined by 11% on average.

The Good News for You: Competition has returned to the market.

- Property Rates: Down 14%.

- Financial Lines: Down 10%.

The Warning: This relief is not universal. If you hold “challenging risks”, such as heavy motor fleets, assets in cyclone zones, or strata schemes with defects, you are likely excluded from these discounts.

## 2. Which Sectors Are Still Considered “High Risk”?

While standard premiums are stabilising, insurers are strictly limiting capacity for high-hazard sectors.

Bellrock Advisory’s Insurance Market Overview (Jan 2025) warns that specific “distressed” assets still face intense scrutiny and limited options. You will face a harder market if you operate in:

- Complex Property (e.g., recycling, textiles, EPS panel construction).

- Strata with Defects (active structural issues).

- Food & Beverage (high fire load risks).

Is Your Business Ready?

The world is entering a more complex risk era. For Australian businesses, navigating these threats requires clarity, context, and expert support.

Are you ready for the 2026 risk landscape? If you are reviewing your business, property, or liability cover, Tank Insurance can help you understand your options and compare insurers.

Contact Tank Insurance or request a quote today.

.